Geopolitical Risk Premium

TLDR: The U.S.-Israeli strikes that killed Khamenei on February 28 have triggered the most significant oil supply disruption risk since Russia’s invasion of Ukraine. Brent will reprice sharply on Monday as Hormuz transit freezes up — potentially toward $100 in the longer term if the strait remains contested. Higher gas prices from the disruption pose a direct threat to the GOP ahead of the November midterms. And Iran’s succession vacuum — with no clear heir and rival Islamic Revolutionary Guard Corps (IRGC) factions jockeying for power — makes the medium-term outlook unusually binary: either a friendlier Iran that floods the market with cheap oil or a leaderless state that keeps the risk premium elevated indefinitely.

Oil: Expect a Sharp Spike — and Possibly a Long Tail

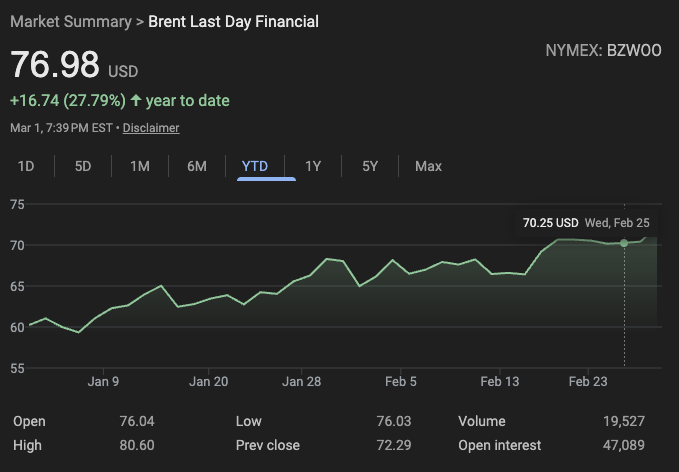

Oil closed Friday at $73 ($77 as of 3/1) — already about $10 above where supply-demand fundamentals would justify. Monday’s open will be ugly. The Strait of Hormuz carries roughly 15 million barrels per day, and Iran’s IRGC declared it closed to shipping late Saturday. At least five supertankers reversed course on February 28. Insurers are canceling coverage for vessels in the area. Even if the U.S. Navy clears a formal blockade quickly, satellite jamming and mines make the passage hazardous in the near term. Saudi and UAE pipelines can bypass Hormuz but only partially — 8-10 million b/d would still be stranded. OPEC raised output only modestly at its March 1 meeting.

Oil closed Friday at $73 ($77 as of 3/1) — already about $10 above where supply-demand fundamentals would justify. Monday’s open will be ugly. The Strait of Hormuz carries roughly 15 million barrels per day, and Iran’s IRGC declared it closed to shipping late Saturday. At least five supertankers reversed course on February 28. Insurers are canceling coverage for vessels in the area. Even if the U.S. Navy clears a formal blockade quickly, satellite jamming and mines make the passage hazardous in the near term. Saudi and UAE pipelines can bypass Hormuz but only partially — 8-10 million b/d would still be stranded. OPEC raised output only modestly at its March 1 meeting.

Energy equities and oil-linked instruments will reprice sharply. If Hormuz transit remains contested, the Economist notes prices could push toward $100. If this resolves quickly — U.S. forces clear the strait and retaliation fades — the pre-existing supply glut (the IEA projected a 3.7 million b/d surplus for 2026) reasserts itself. But if Iran sustains chaos through mines, drone attacks on Gulf infrastructure or strikes on neighboring oilfields, an $8-12/barrel risk premium could persist for months. The Dallas Fed’s rule of thumb: a $10 increase in Brent lifts gasoline by roughly 25 cents per gallon within days. The Strategic Petroleum Reserve (SPR) at 415 million barrels offers about three months of buffer at maximum draw — not enough if this drags out.

Midterms: Higher Pump Prices Are the GOP’s Biggest Domestic Risk

Americans vote in November, and the Republican Party is already underwater on cost-of-living issues. Gasoline prices are one of the most viscerally felt economic indicators, meaning a sustained spike would compound the problem for the Republicans. The asymmetry here is of particular concern: pump prices rise fast when crude goes up but fall slowly when it comes back down. Even a short-lived oil shock could leave elevated gas prices lingering through the summer driving season and into the fall campaign.

Americans vote in November, and the Republican Party is already underwater on cost-of-living issues. Gasoline prices are one of the most viscerally felt economic indicators, meaning a sustained spike would compound the problem for the Republicans. The asymmetry here is of particular concern: pump prices rise fast when crude goes up but fall slowly when it comes back down. Even a short-lived oil shock could leave elevated gas prices lingering through the summer driving season and into the fall campaign.

Trump could tap the SPR to blunt the impact — Biden did this after Russia invaded Ukraine — but the reserve is now 27% smaller. The political calculation is straightforward: the faster this campaign achieves its objective (whatever that might be), and Hormuz reopens the better the electoral prospect for the Republican Party. A prolonged conflict keeping oil elevated through Q3 would be a serious midterm liability.

Iran’s Succession: A Dangerous Vacuum

Khamenei’s death leaves Iran without a clear successor for the first time since the Islamic Republic’s founding. A three-person interim council (president, judiciary chief, and a Guardian Council member) will hold temporary authority while the 88-member Assembly of Experts selects a new supreme leader. But the real power dynamics will play out behind the scenes.

The leading candidates each carry liabilities. Alireza Arafi could bridge factional divides but lacks a power base. Mohseni-Eje’i heads the judiciary but is despised by the public. Mojtaba Khamenei has intelligence connections but thin religious credentials. Meanwhile, Ali Larijani — a pragmatist and former nuclear negotiator now running the Supreme National Security Council — is positioned as a key power broker.

The critical variable is the IRGC. Iran’s military hierarchy proved remarkably resilient last summer when some 30 top commanders were killed without disrupting operations. But without a strong supreme leader to arbitrate between rival IRGC factions, the risk of internal fragmentation remains.

Investment implication: This creates a binary outcome set. If pragmatists gain influence and move toward de-escalation, sanctions relief and rising Iranian exports could reinforce the supply glut and push oil well below $60. If hardliners consolidate — or factional infighting produces chaotic governance — Iran will be a source of instability and buyers like China face uncertainty about who controls the spigots. The regime’s survival threshold is higher than that of most regional states. Unfortunately, I do not foresee a quick resolution in either direction.

Comments